FSA prepares for 'unprecedented task' of resuming student loan payments after forbearance

The coronavirus pandemic led to a payment pause on federal student loans, but that temporary relief has a definitive end date of Jan. 31, 2022. See how you can prepare for when payments restart in February. (iStock)

Federal student loan payments have been paused since the CARES Act was signed into law in March 2020, but the suspension of loan payments is coming to an end in just a few months.

The office of Federal Student Aid (FSA) is now preparing for the "unique and unprecedented task" of returning 25 million borrowers into repayment, FSA Chief Operating Officer Richard Cordray said at a conference on Sept. 16, according to prepared remarks obtained by Politico.

Cordray mentioned that the stakes are "extremely high" for borrowers who rely on COVID-19 emergency relief measures as a lifeline. "This is a defining moment, and it is important that we get it right," he said.

A large part of that is a communications campaign that includes a series of emails directly sent to borrowers, social media messaging and updates to the FSA website. The goal is to prevent delinquencies and defaulted loans when the payment pause ends.

SENATE CONFIRMS JAMES KVAAL AS UNDER SECRETARY OF EDUCATION

No matter what the FSA and the Department of Education do to prepare for payments to resume, it doesn't change the fact that many borrowers are still not ready for forbearance to end. In fact, 40% of borrowers said in a recent survey that they need federal student loan deferment to be extended beyond February 2022.

Keep reading to learn how you can apply for additional forbearance, enroll in an income-driven repayment plan (IDR plan) or lower your student loan payments by refinancing. If you decide to refinance, compare offers from multiple private lenders without impacting your credit score on Credible.

How to prepare for student loan payments to resume

The final extension of federal student loan forbearance runs through January 2022, which means that payments will automatically restart in February 2022. Here are a few things you can do in the coming months to prepare for the end of forbearance.

WARREN SAYS PRESIDENT BIDEN 'HAS THE POWER TO CANCEL STUDENT LOAN DEBT'

Refinance to a lower rate to reduce your monthly payments

Private student loan refinancing is when you take out a new student loan with better terms to repay your current student loans. You may be able to lower your monthly payments, pay off your debt faster and even save money on interest over the life of the loan by refinancing to a lower interest rate.

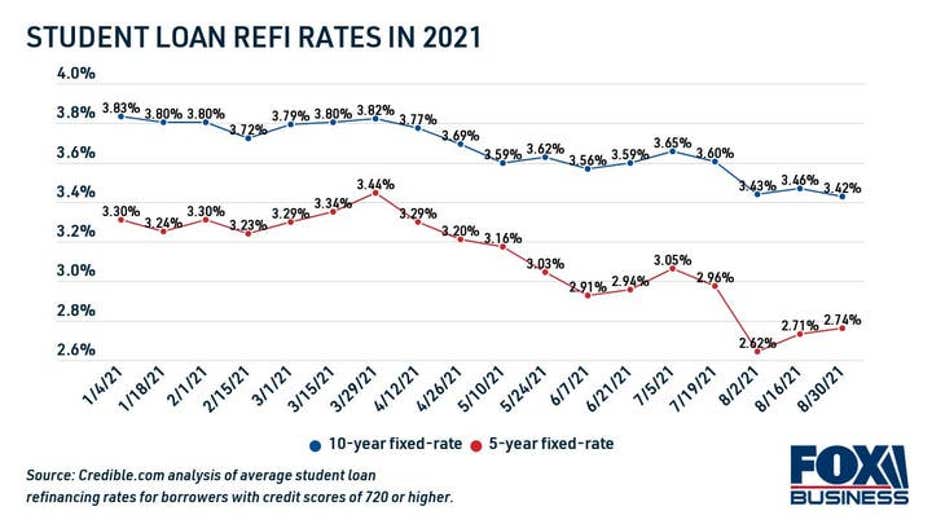

Student loan rates are near historic lows, according to data from Credible, which makes it possible for borrowers to save thousands of dollars on their student loans by refinancing.

There's one caveat: Refinancing your federal loans into a private student loan makes you ineligible for federal protections like income-driven repayment, administrative forbearance and student loan forgiveness programs. It may not be worth refinancing to a lower rate if you plan on applying for any of these federal benefits.

You can browse student loan refinance rates from real private lenders in the table below. Visit Credible to see student loan refinance offers tailored to you for free.

BIDEN ADMINISTRATION LAUNCHES INQUIRY TO FIX PSLF PROGRAM

Enroll in an income-driven repayment plan

Federal student loan borrowers may be eligible to limit their monthly student loan payments to a portion of their income by enrolling in income-driven repayment (IDR). The FSA offers four different IDR plans, depending on the type of federal student loans you have:

- Revised Pay As You Earn Repayment Plan (REPAYE Plan)

- Pay As You Earn Repayment Plan (PAYE Plan)

- Income-Based Repayment Plan (IBR Plan)

- Income-Contingent Repayment Plan (ICR Plan)

Your student loan payments will be limited to about 10-20% of your discretionary income based on the type of IDR plan you have. See the qualifications and enroll in an IDR plan on the FSA website.

98% OF PUBLIC SERVICE LOAN FORGIVENESS APPLICATIONS REJECTED

Apply for additional economic hardship forbearance

When the federal student loan forbearance period ends, you may be eligible for an extended deferment period of up to 36 months through the Education Department. Apply for unemployment deferment or economic hardship deferment on the FSA website.

You can also apply for forbearance on your private student loans, but keep in mind that each lender sets its own parameters and eligibility requirements for forbearance. Learn more about student loans, including forbearance and refinancing, by getting in touch with a knowledgeable loan officer at Credible.

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.